The Uncertainty of War

The one thing that is certain when geopolitical events take hold is that uncertainty runs rife, and the one thing that investors and the markets don’t like is uncertainty. It’s during these times that market volatility picks up and emotional investors tend to head for the exit. But with so many factors at play in addition to the increase in geopolitical risk –high inflation, Central Banks removing accommodative policies, and the possibility of another Covid variant to emerge to name a few – investors should ask themselves, ‘Is now the time to give up on a well-diversified portfolio?’

What can we learn about the markets’ reaction to historical geopolitical tensions?

Uncertainty from geopolitical tensions creates worry, and during these times risk assets tend to sell off. But the fall and negative impact on risk assets, while significant at times, has always proven to be temporary. During a geopolitical event, the perceived safe assets of gold and US Treasuries have held up best, while risk assets, namely equities, can fall into correction territory –historically registering a drop of at least 10%.

Asset Class reaction to geopolitical events (Cumulative return %)

Source: Schroders Wealth Management, “Measuring the impact of geopolitics on markets”, 10/10/2019

As time moves forward, markets assess the risk and adjust their expectations, generally leading to a strong rebound within a few months. Using the above geopolitical examples, the Gulf War saw equities rise 5 months after it began, while the 9/11 Terrorist Attacks and the Iraq War saw the market rebounding after 2 and 3 months, respectively¹.

Expanding the data set to include 29 geopolitical crisis events around the globe starting with World War II, it was found that the US equity market was on average 2% higher 3 months after an event. For the six-month period, 69% of the 29 events saw a higher equity market with an average return of 5%².

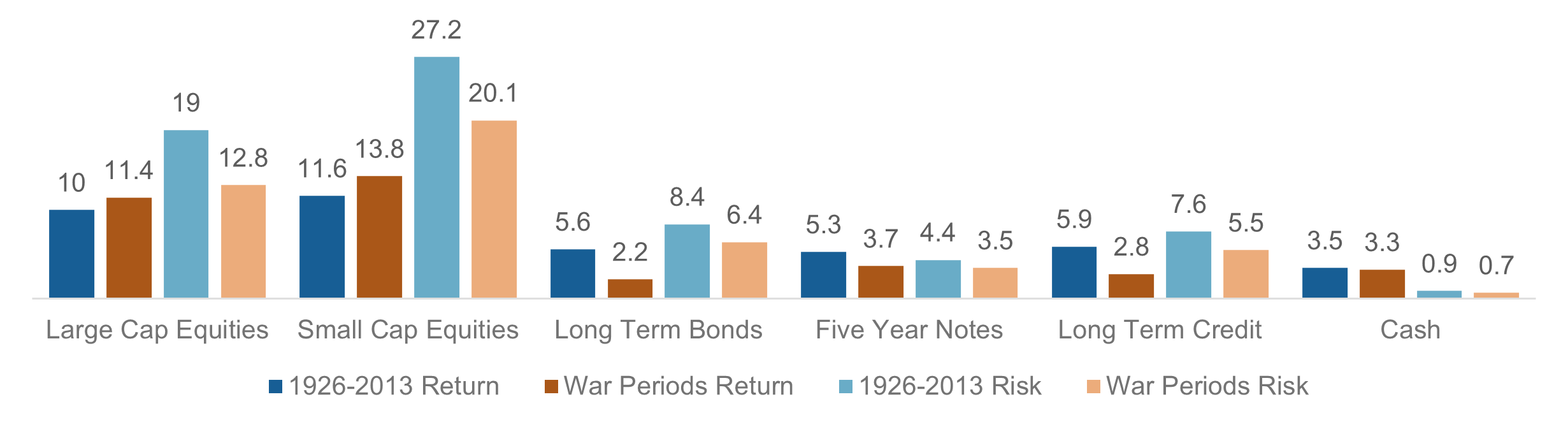

One counterintuitive observation that was made when looking specifically at US war periods (World War II, Korean War, Vietnam War and Gulf War) vs long-term historic averages (1929 – 2013), was that on average, the volatility of asset classes was lower during the war periods than for the full period. Equities on average saw higher returns during war periods than during the full period, and were higher than both bonds and cash³. In contrast, bonds saw lower returns than the full period partially due to the higher levels of inflation seen during times of war, and increased government borrowing that saw yields rise and prices fall. Inflation during war periods was on average 4.4% compared to 3.0% for the full period.

Capital Market Performance During Times of War (Annualized Return / Risk - %)

Source: CFA Institute – Mark Armbruster, “What Happens to the Market if America Goes to War”, August 29, 2017

What impact will the Russian invasion of Ukraine have on the economy?

With sanctions being applied to Russia as a result of its invasion of Ukraine, the biggest loser will probably be Russia and could potentially push the nation into recession. If that were to happen it will likely have minimal effect on the markets and global economy. Due to its demographic trends and weak productivity, Russia has not grown much over the past few years and comprises just 4% of the Emerging Market index and represents 1.8% of global GDP⁴. The bigger impact will be around commodities, the potential impact on inflation and how that might affect Central Bank activity.

Representing nearly 20% of world exports in gas and wheat and 10% of world exports in copper and aluminum, sanctions on Russia could lead to supply shortages in these areas impacting commodity, food and oil prices⁵. This will likely keep inflation elevated for longer, with the inflation impact being seen most in those countries that have closed output gaps and have seen stronger recoveries from the pandemic, which includes the US.

While not expected to tip the global economy into recession, this will likely lead to a slow-down in growth which is already expected to experience a fall from over 6% in 2021 to just over 4% in 2022. Central Banks will have a delicate act to balance the slowing growth, while seeing high inflation. With the US being a little more insulated from the impacts of higher oil prices due to its own production, expectations are that the Federal Reserve will not aggressively respond to the higher prices and focus more on the stability of the economy. The Federal Reserve will likely continue to raise rates but will do so in a measured and slow rate, as it seeks to limit any shocks to the system.

Conclusion

Geopolitical tensions always remind us that there are unpredictable shocks that affect the markets, and the resulting volatility shows that the market is functioning in a normal manner. With so many varied factors potentially impacting the markets, trying to time what type of assets to hold is a fool’s game. While you may have timed getting out of the markets correctly, the timing of getting back in might be harder and your portfolio could potentially miss out on return potential, as some of the largest returns in the markets are typically seen after significant falls. Remaining diversified across multiple asset classes – some for risk taking, some for defensiveness, some for income – should allow a portfolio to benefit at any market turn.

[1] Schroders Investment Management - Measuring the Impact of Geopolitics on Markets

[2] Glenview Trust Company - Geopolitical Events and Stocks

[3] CFA Institute - What Happens to the Market if America Goes to War?

[4] Ned Davis Research - Global Asset Allocation in a Volatile Market Environment

[5] Ned Davis Research - What Russian Sanctions Mean for the Global Economy

Check the background of your financial professional on FINRA's BrokerCheck.

The content is developed from sources believed to be providing accurate information. The information in this material is not intended as tax or legal advice. Please consult legal or tax professionals for specific information regarding your individual situation. The opinions expressed and material provided are for general information, and should not be considered a solicitation for the purchase or sale of any security.

This communication is strictly intended for individuals residing in the states of AL, CA, FL, IN, MT, NC, OH, TX, WA, WV. No offers may be made or accepted from any resident outside these states due to various state regulations and registration requirements regarding investment products and services. Securities and Advisory Services Offered Through Commonwealth Financial Network (Privacy Policy), Member FINRA/SIPC and a Registered Investment Advisor, Fixed Insurance Products and Services Offered Through CES Insurance Agency.

IMPORTANT INFORMATION

This report is for informational purposes only, and is not a solicitation, and should not be considered as investment or tax advice. The information has been drawn from sources believed to be reliable, but its accuracy is not guaranteed, and is subject to change.

Investing involves risk, including the possible loss of principal. Pas performance does not guarantee future results. Asset allocation alone cannot eliminate the risk of fluctuating prices and uncertain returns. There is no guarantee that a diversified portfolio will outperform a non-diversified portfolio in any given market environment. No investment strategy, such as asset allocation, can guarantee a profit or protect against a loss. Actual client results will vary based on investment selection, timing, and market conditions. It is not possible to invest directly in an index.

Information presented here has been developed by an independent third party, AssetMark, Inc.

AssetMark, Inc. is an investment adviser registered with the Securities and Exchange Commission. (C)2022 AssetMark, Inc. All rights reserved.